F-14/15, Orbit Mall, Civil Lines, Jaipur-302006

F-14/15, Orbit Mall, Civil Lines, Jaipur-302006 support@thetaxheaven.com

support@thetaxheaven.com

F-14/15, Orbit Mall, Civil Lines, Jaipur-302006 support@thetaxheaven.com

Choosing between a Credit Card and a Personal Loan in 2026 requires a clear focus on cost. Many borrowers compare convenience or speed, but interest cost determines how much you repay over time. While both are credit facilities, they differ at functional levels. Each option follows a different pricing structure, which affects the total amount you pay.

A Credit Card offers flexibility through revolving credit, but it can quickly increase costs if you carry a balance past the due date.

● Unpaid balances: Lenders charge interest on any outstanding amount that remains unpaid after the billing cycle ends.

● Daily interest calculation: Most Credit Card providers calculate interest daily, which steadily increases the total payable amount.

● Minimum payments: Paying only the minimum due extends the repayment period and increases the overall interest paid.

● Rolling balances: Carrying balances across multiple cycles leads to compounding, significantly increasing costs over time.

This structure makes Credit Cards expensive when you use them beyond short-term transactions.

A Personal Loan provides a fixed amount with a clear repayment schedule. When you get a Personal Loan, you agree to repay it through fixed installments over a defined period.

● Fixed disbursal: The borrower receives a lump sum at the start of the loan tenure.

● Reducing balance method: Lenders calculate interest only on the remaining principal, which reduces with each payment.

● Fixed instalments: Monthly payments remain constant, which helps with financial planning.

● Defined tenure: Borrowers can choose a repayment period between 6 to 60 months (available in blocks of 6, 12, 18, 24, 30, 36, 42, 48, 54 or 60 months), which determines the total interest payable.

Personal Loans, such as those offered by HSBC Bank (available exclusively to existing HSBC customers), use a fixed repayment schedule, allowing borrowers to estimate the total cost in advance.

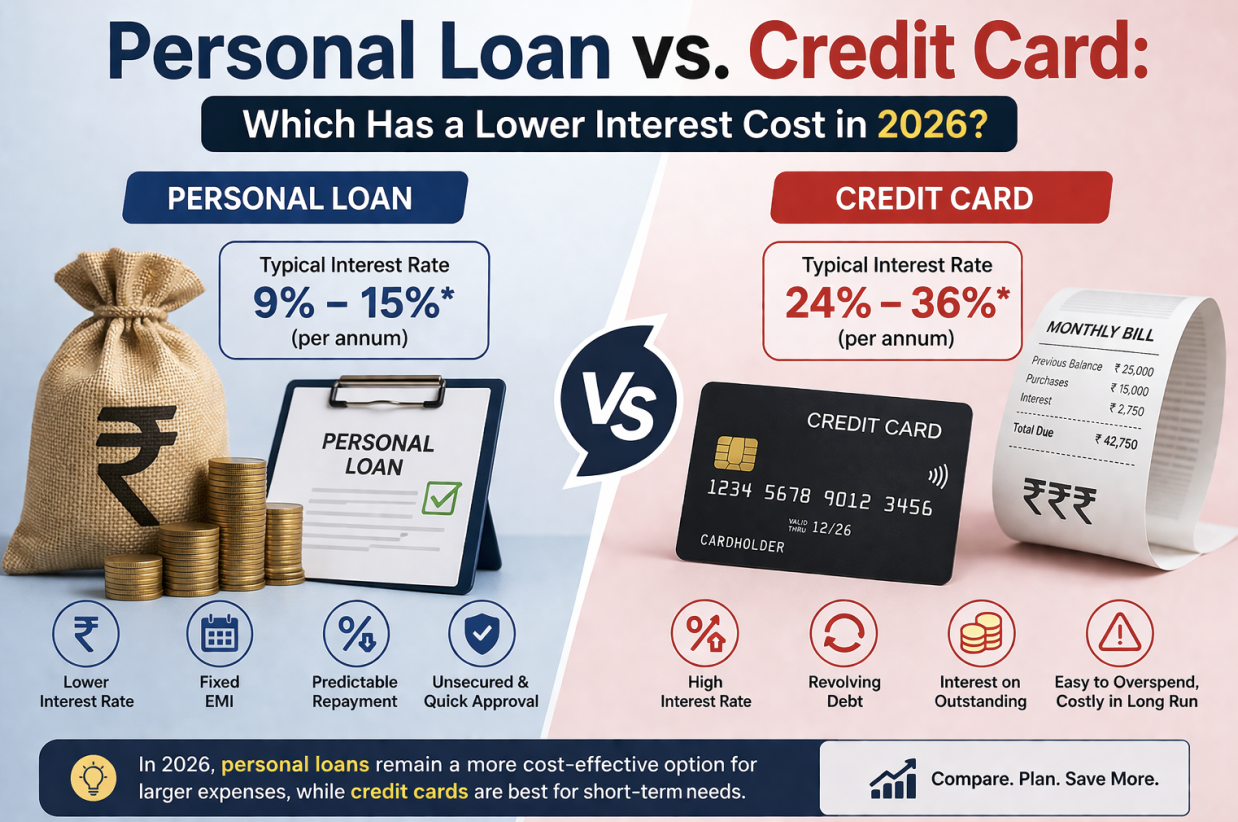

Which Option Typically Has Lower Interest Cost

Since the two options differ in functionality, you cannot compare their final costs. If you want to manage your monthly expenses on a routine basis, a Credit Card can be a favourable choice. You can repay the bill within the billing cycle without paying anything extra. Whereas, a Personal Loan is ideal for any sudden financial need, such as a medical emergency, home repair, travel plan, higher education cost, etc. The total interest cost depends on how interest accumulates and how long the borrowed amount remains unpaid.

● Credit Cards: These usually carry higher interest rates when balances are not paid in full each month.

● Personal Loans: These generally offer lower interest rates and a fixed repayment plan.

For borrowing that continues over several months, Personal Loans often result in a lower total interest cost than revolving credit, especially when repayments remain consistent and timely throughout the loan tenure.

Credit Cards can remain cost-efficient when you use them with discipline and repay on time.

● Interest-free period: Most Credit Cards provide a grace period during which no interest applies if you clear the full balance.

● Full repayment habit: Paying the entire statement amount before the due date eliminates interest charges completely.

● Short-term use: Using a Credit Card for short-term expenses avoids long-term borrowing costs.

In such cases, Credit Cards function as a convenient and cost-free payment method.

Personal Loans suit situations where you need fixed repayment for larger expenses. When you review the eligibility for a Personal Loan, you can assess whether this option fits your financial position.

● Large expenses: A Personal Loan allows you to spread costs across several months through fixed payments.

● Lower interest burden: Fixed rates reduce uncertainty and limit the total interest paid over time.

● Disciplined repayment: A fixed schedule encourages consistent repayment behaviour.

If you plan to get a Personal Loan, you can manage repayment more effectively than carrying high-interest Credit Card balances over time.

Several factors influence the interest rate and total cost of borrowing. Your eligibility for a Personal Loan plays an important role in determining the final terms.

● Credit score: A strong credit profile helps you secure lower interest rates.

● Loan tenure: Shorter tenures reduce the overall interest paid, even if monthly payments increase.

● Repayment history: Consistent and timely payments improve your borrowing profile.

● Loan amount: Higher loan amounts may affect the rate offered based on risk assessment.

Managing these factors helps you reduce borrowing costs, secure better financial terms, and improve your overall financial stability over time.

The option with the lower interest cost depends on how you use and repay the borrowed amount. Credit Cards work well for short-term spending when you clear the balance in full each month. However, Personal Loans usually offer a lower total interest cost for larger expenses that require fixed repayment. By understanding how interest applies and assessing your repayment ability, you can choose the option that keeps your borrowing cost under control and supports your financial stability.

Register & Login

Register & Login