F-14/15, Orbit Mall, Civil Lines, Jaipur-302006

F-14/15, Orbit Mall, Civil Lines, Jaipur-302006

Register & Login

Register & Login

Efficient financial planning encompasses more than just handling income tax. It involves smart investment choices, including life insurance and tax-saving options. Apart from income tax, the government also gathers indirect taxes like TDS, TCS, and GST on goods, services, and transactions. While earners pay direct taxes, sellers shoulder the responsibility for indirect taxes. (Tax Deducted at Source) and TCS (Tax Collected at Source), often muddled, are essential indirect tax components. For an in-depth grasp of the disparities between TDS and TCS and their impacts, explore the specifics provided below.

Tax Deducted at Source (TDS) and Tax Collected at Source (TCS)

Both TDS and TCS are imposed at the source of income in India.

- TDS refers to the tax deducted by a company on payments to an individual that exceed a specified limit. On the other hand, TCS represents the tax collected by sellers during transactions with buyers.

- TDS deduction is relevant for various payments including salaries, rent, professional fees, brokerage, commission, etc. On the other hand, TCS deduction applies to the sale of goods such as timber, scrap, mineral wood, and similar items.

- TDS applies solely to payments that surpass a specified threshold, whereas TCS is relevant to the sales of certain goods, excluding production or manufacturing materials.

Key Differences Between TDS and TCS

You can understand the difference between TDS and TCS through the following illustration:

|

Parameters |

TDS |

TCS |

|

Transactions Covered |

TDS covers various expenses including interest, salaries, brokerage commission and rent. |

TDS is applicable on sale of goods like timber, minerals, alcoholic beverages and toll plazas. |

|

Responsibility for Tax Collection or Deduction |

A source tax is deducted by the payer when he or she makes a defined payment to another person (deductee), and it is returned to the Central Government. Moreover, TDS exemption can be availed by submitting Form 26AS (TDS certificate). |

The seller's only responsibility is to collect TCS from the buyer and remit it to the Central Government. |

|

Limits |

Section 194Q imposes a TDS on goods purchased over ₹50 lakhs. |

The levy of TCS is required on the sale of goods whose value exceeds ₹50 lakhs, as per Section 206C(1H). |

|

Tax Deduction or Collection Period |

TDS is taken out whenever a payment is made, regardless of when it becomes due. |

On the other hand, TCS is collected at the time of sale by the seller. |

|

Returns Filing |

Quarterly

|

Quarterly

|

|

Due Date for Payment to the Government |

The due date for depositing TDS is the 7th of every month. Note that TDS returns are required to be submitted quarterly. |

Per the rules, TCS will be deducted during the month the supply is made. Note that it will be deposited within ten days from the end of the month of supply to the government's credit. |

Also Read - TDS Return Forms - Form 24Q, 26Q, 27Q, 26QB, 26QC, 27EQ & Find TDS Due Date

Tax Deducted at Source (TDS) and Tax Collected at Source (TCS) with Examples

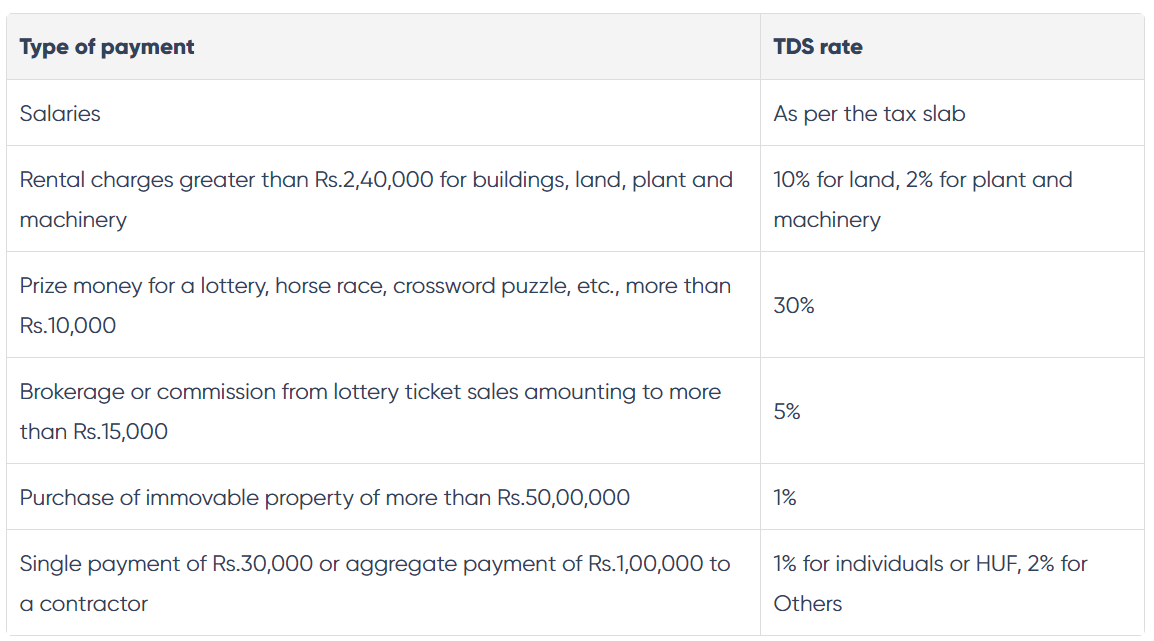

Example for TDS

Consider Mr. X, an employee at a company. Before disbursing his monthly salary, the company deducts taxes at the applicable rate, known as TDS.

TDS rates for some payment types

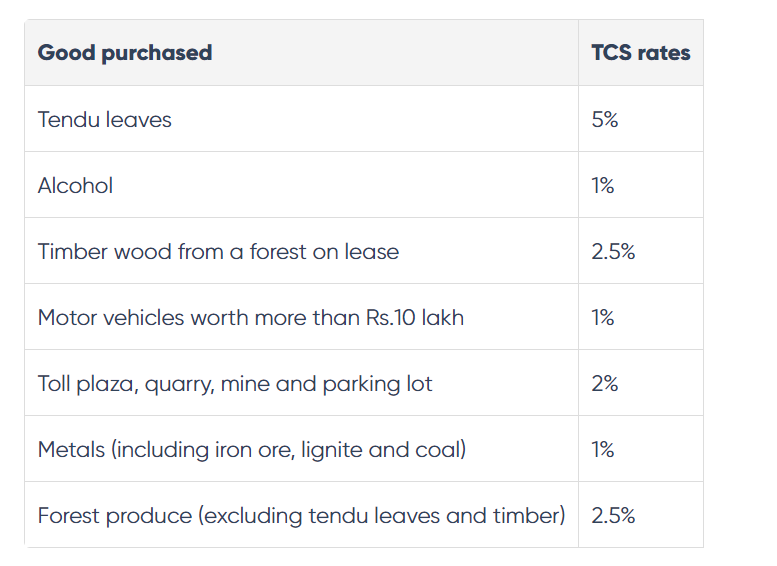

Example for TCS

Conversely, Mr. Y, a mineral wood trader, collects 5% tax from his customer, Mr. Z, during the wood sale. This amount collected by Mr. Y from the buyer is referred to as TCS.

TCS rates for some commonly bought goods

Difference between TDS/TCS under GST

Tax Deducted at Source (TDS) and Tax Collected at Source (TCS) are pivotal aspects of the Goods and Services Tax (GST) framework in India, yet they serve distinct purposes.

- TDS is deducted by the recipient of goods or services at a specified rate while making payments to the supplier above a certain threshold, ensuring tax compliance. It is a mechanism to stabilize revenue and monitor transactions.

- Conversely, TCS is collected by the seller while selling certain goods or services and is deposited with the government. It is aimed at facilitating proper tax collection and preventing tax evasion.

- While TDS focuses on deduction by the buyer, TCS emphasizes collection by the seller, both contributing significantly to the tax structure under GST. Understanding the nuances between TDS and TCS is vital for businesses to ensure adherence to GST regulations and maintain smooth financial operations.

Impact on Parties Involved

Impact on Payer/Deductor

1. TDS - Reduces cash flow at the time of payment

When it comes to TDS, the payer or deductor faces the immediate impact of reduced cash flow at the time of payment. This means that a certain percentage of the payment made to the payee is withheld as tax and remitted to the government. While the intention behind TDS is to ensure proper tax compliance, it can pose a significant challenge for the payer, especially if they have multiple payments to be made. The deducted tax affects their available funds, potentially disrupting their cash flow and liquidity.

2. TCS - Increases selling price, impacting competitiveness

On the other hand, TCS has a different effect on the payer or deductor. When tax is collected at the source, the selling price of goods or services increases, impacting the overall competitiveness of the payer in the market. This is because the collected tax is eventually passed on to the end consumer, making the product or service relatively more expensive compared to those not subject to TCS. This can become a concern for businesses trying to attract customers and stand out in a competitive landscape.

Impact on Payee/Supplier

1. TDS - May claim credit for deducted tax

For the payee or supplier, TDS brings about both challenges and opportunities. One of the positive aspects is the ability to claim credit for the tax deducted at source. This means that the amount withheld as tax can be adjusted against the payee's overall tax liability. By claiming this credit, the payee can potentially reduce their tax burden and ensure compliance with the tax regulations. However, this process may involve additional paperwork and verification, adding complexity to their financial management.

2. TCS - Needs to adjust for the collected tax in pricing

In the case of TCS, the payee or supplier needs to make adjustments in their pricing to account for the tax collected at source. This can be a delicate balancing act, as they aim to maintain their competitiveness while still complying with the tax regulations. Adjusting the pricing to include the collected tax may require careful calculations and consideration of market dynamics. Failure to accurately account for the collected tax can lead to potential losses or penalties, further highlighting the challenges faced by the payee.

Penalties and Consequences

TDS Non-Compliance

1. Interest on late payment

Late payment of Tax Deducted at Source (TDS) can attract significant interest penalties. The purpose of TDS is to ensure the smooth collection of taxes from various sources of income. It is the responsibility of the deductor, whether an individual or a company, to deduct TDS and remit it to the government within the stipulated time frame. Failing to do so can have financial implications.

If the TDS is not paid on time, an interest penalty of 1% per month or part thereof is levied. This can quickly add up, especially if the delay continues over a prolonged period. The interest calculation starts from the date on which the TDS should have been deposited and continues until the actual date of payment. Therefore, it is essential for deductors to ensure timely payment to avoid unnecessary burden.

2. Penalties for non-deduction or late filing

Non-deduction or delayed filing of TDS can also lead to penalties. The Income Tax Act prescribes penalties for non-compliance, which vary based on the severity of the offense. If a deductor fails to deduct TDS, a penalty equal to the amount of tax that should have been deducted is imposed. Furthermore, if the TDS is deducted but not deposited within the due date, a penalty ranging from 100% to 300% of the withheld amount may be levied.

Late filing of TDS returns can attract penalties as well. The penalty for delay in filing a TDS return is Rs. 200 per day of default. However, the total penalty amount cannot exceed the total amount of TDS deducted. This can be a substantial blow to taxpayers who fail to comply with the filing deadlines.

TCS Non-Compliance

1. Consequences for not collecting tax at source

Similar to TDS, Tax Collected at Source (TCS) also carries consequences for non-compliance. TCS is applicable on certain transactions, such as purchase of specified goods or services, where the seller collects the tax from the buyer. Failure to collect TCS can have serious repercussions.

If TCS is not collected, the seller becomes liable to pay the TCS amount from their own funds. This can lead to financial strain, especially if the seller has already transferred the goods or services without collecting the tax. The seller may also be subject to penalties for non-compliance.

2. Penalties for non-compliance

Non-compliance with TCS regulations can result in penalties. The penalty for not collecting or non-remittance of TCS can be a daunting 100% to 300% of the TCS amount. The exact penalty depends on the duration of the non-compliance and the gravity of the offense. These penalties are meant to discourage individuals and businesses from evading their tax collection responsibilities.

It is important to note that penalties may vary based on the provisions of the Income Tax Act and any subsequent amendments. To ensure compliance and avoid penalties, it is crucial for sellers to stay updated with the latest legal requirements and fulfill their TCS obligations in a timely manner.

Remember, it is always better to fulfill your tax obligations diligently and on time to avoid any financial and legal repercussions!

In The Final Analysis

One of the most crucial facets of managing a successful business is staying on top of your tax obligations. To keep your business operating smoothly, it is essential to understand the TDS and TCS difference and make sure you pay any TDS or TCS you have collected to the government's credit. In addition, if taxes are deducted from your pay, make sure to file your taxes on time.

Frequently Asked Questions (FAQs)

Q. What is TDS (Tax Deducted at Source)?

Tax Deducted at Source (TDS) is a scheme in which the tax is collected at the source. During this process, TDS is deducted and paid to the Central Government whenever one taxpayer pays another.

This concept of deducting and paying ensures that tax is collected by the payer of income and that income is offered for taxation by the recipient. Thus, taxes are collected beforehand and the central government tracks incomes When filing an income tax return, one may claim TDS. The rate of TDS varies on kinds of incomes, types of taxpayers, and place of residence of a taxpayer.

Q. What is TCS (Tax Collected at Source)?

TCS mandates that the seller of goods oversees tax collection from the purchaser of said goods. The seller deposits the money to the national government's credit after collecting the tax.

Collection incidents occur when receiving sales proceeds or debiting accounts, depending on which occurs first. Section 206C of the Income Tax Act, 1961 lists the items subject to TCS. These include wood, alcohol, lignite, and coal, as well as parking lots and toll booths. TCS is only allowed to sell goods up to a maximum of ₹50 lakhs.

Q. Can TCS be adjusted against TDS?

Ans. TDS is applicable on an income other than the sale of goods like commission, professional fees, salary, and so on. Can TCS be adjusted with TDS? No, TCS cannot be adjusted against TDS and vice versa. The point of collection and deduction are very different.

Q. What if TDS and TCS both are applicable?

Ans. As per Circular No. 13/2021, if, for any reason, TCS has been collected by the seller u/s 206C(1H) of the Act, before the buyer could deduct TDS u/s 194Q of the Act on the same transaction, such transaction would not be subjected to TDS again by the buyer.

Q. What happens when individuals fail to deposit or collect tax?

There are legal consequences for failing to collect or deposit tax. This could include

- A penalty amount equal to the tax which is not deducted or collected

- Imprisonment of three to seven years plus fine

- An interest on the monthly tax amount eligible for deduction. This interest applies for each month from the day when the tax becomes eligible for deduction to the day when it is deducted (at the rate of 1 percent) or when it is paid to the government (at the rate of 1.5%). In case of the TCS, the interest rate remains 1%.

Q. Can I collect TCS if TDS is already deducted?

Yes, TCS can be collected even if TDS is already deducted. Both TDS and TCS are distinct provisions under the tax system, where TDS is deducted by the buyer while making payments to the seller, whereas TCS is collected by the seller from the buyer during the sale of specified goods or services. Therefore, both TDS and TCS can coexist in a transaction, as they serve different purposes and apply to different aspects of taxation.

Q. What is the time limit for a TDS refund?

The time limit for a TDS refund is generally within a period of one to six months from the date of filing an income tax return. The Income Tax Department endeavors to process and issue refunds expeditiously. However, the actual duration may vary based on several factors, including the accuracy of the filed return, verification processes, and workload at the department. Taxpayers can track their refund status through the Income Tax Department's online portal or through the Tax Information Network (TIN) facilitation centers.

Q. What is TDS on salary?

TDS on salary is when employers deduct taxes from employees' pay based on their income tax slabs and allowances, depositing this deducted amount to the government on behalf of the employee.

Q. Is TCS applicable if TDS is deducted?

Yes, TCS is still applicable even if TDS (Tax Deducted at Source) has been deducted. Both TCS and TDS are separate tax provisions applicable in different scenarios and transactions in India's taxation system.

Q. What is TDS and TCS amount?

TDS and TCS amounts differ based on income types and sales. They are calculated as per government-set rates in the Income Tax Act (TDS) and GST regulations (TCS).

Q10. Who will deduct TDS and TCS?

TDS is deducted by individuals or entities making payments exceeding a specified limit, as per the Income Tax Act. TCS is collected by sellers or traders during certain transactions, mainly for specific goods. These processes ensure tax compliance and revenue collection as per Indian tax regulations.