F-14/15, Orbit Mall, Civil Lines, Jaipur-302006

F-14/15, Orbit Mall, Civil Lines, Jaipur-302006

Register & Login

Register & Login

Section 194-I outlines the rules for deducting tax at source (TDS) on rent. This applies to those earning income from rent or subletting. The TDS applies as rent is additional income for business people, salaried individuals, and others.

This guide is aimed at individuals paying rent for land, buildings, or various equipment.

Section 194I Overview

- Non-individuals or HUFs paying rent must deduct tax at source.

- The tax deduction threshold for rent is Rs 2,40,000 for FY 2022-23 (previously Rs. 1,80,000 until FY 2018-19).

- Individuals and HUFs subject to tax audit must also deduct tax at source.

- Tax on rent must be deducted at the time of rent payment or credit to the payee's account, whichever comes first.

Why was TDS u/s 194I Introduced?

The Finance Act of 1994 included Section 194I for tax deductions on rent payments. This was implemented to tax rental income at the source, a practice also seen in other countries.

TDS on Rent Conditions

- No surcharge on TDS on rent unless it involves a foreign company and payment exceeds Rs.1 crore.

- The landlord's PAN number is required for TDS deduction. Without it, TDS on rent is deducted at 20% under Section 206AA.

- TDS on rent does not include any Education Cess or Secondary and Higher Education Cess.

Definition of ‘Rent’ as per Section 194I

- 'Rent' refers to any payment, for use of items like:

- Land

- Building (or factory building)

- Land associated with a building (or factory building)

- Machinery

- Plant

- Equipment

- Furniture

- Fittings

- This applies whether or not the payee owns the items. Sub-letting is included.

- No tax deduction is required for security or advance payments collected by a landlord, as these are not deemed income and will be refunded.

- However

TDS Rate

|

No. |

Payment Type |

Tax Deduction Rate |

|

1 |

Plant, equipment and machinery rent |

2% |

|

2 |

Land, building, furniture or fitting rent |

10% |

Covered Payments under Section 194I

- Rent from Factory Building

If a factory building is rented out, the rent is usually a business income for the lessor or owner. This is subject to tax deduction at source (TDS).

- Inclusive of Service Charges

Service charges from business centres are included as rent.

- TDS for Separate Building and Furniture Rentals

If a building and furniture are rented by different people, tax needs to be deducted from the building rent only under Sec. 194I.

- TDS on Non-Monthly Rent Payments

Under Sec. 194I, TDS is not required to be deducted monthly. It can be done quarterly or yearly based on the payment schedule.

- Cold Storage Facility Charges

Payments for cold storage facilities are considered as charges for plant use, not building use.

- Association Hall Rent

Associations have tax deduction obligations if the hall

Table of Contents

- Section 194I Overview

- Why was TDS u/s 194I Introduced?

- TDS on Rent Conditions

- Definition of ‘Rent’ as per Section 194I

- TDS Rate

- Covered Payments under Section 194I

- Section 194IA Requirements

- How to Pay TDS via Challan 26QB and Get Form 16

- Online e-Payment via Challan 26QB

- Form 26QB Non-filing Notice

- Taxpayer Notice Example

- Form 26QB Filing Requirements

- Form 16B TDS Certificates from TRACES

- Consequences of Non/Late TDS Statements Submission

- Penalties for Non-Filing of Form 26QB

Are you buying a house? Read this article.

Taxes play a crucial role when buying or selling property in India.

A key tax is the Tax Deducted at Source (TDS) associated with property sale under Section 194-IA. This tax applies to immovable property like land and buildings. The buyer deducts this tax before paying the seller. Learn more about TDS on property sale under Section 194IA, who deducts it, and how to file it.

Section 194IA Requirements

A buyer must deduct TDS when buying non-agricultural immovable property worth over Rs 50 lakhs. This is detailed in Section 194-IA of the Income Tax Act since 1st June 2013.

- The buyer must deduct TDS at 1% of the total sale amount. The buyer, not the seller,

- DS needs to be deducted if the total sale price equals or exceeds Rs 50 lakh.

- TDS must be deducted on each instalment

- 'Consideration for immovable' property covers all incidental costs such as club membership, parking, utilities, maintenance, and advance fees. This applies to properties bought on or after September 1, 2019, according to Budget 2019.

- The full sale price must be paid as TDS.For example, if you paid Rs. 55 lakh for a house, you must pay TDS on Rs. 55 lakh rather than Rs. 5 lakh (i.e., Rs. 55 lakh - Rs. 50 lakh). This still holds true if there are multiple buyers or sellers. After the budget 2019 amendment to section 194-IA, if you paid the parking fee of Rs. 2 lakh, the water facility fee of Rs. 1 lakh, and the electricity facility fee of Rs. 1 lakh on September 1, 2019, your sale consideration would be Rs. 59 lakh (55+2+1+1). On Rs 59 lakh @ 1%, you must pay TDS. The amount of TDS you must pay is Rs 59,000.

- No need for a TAN (Tax Deduction Account Number) to deposit TDS for property purchase. Use your PAN to make the payment.

- Buyers must get the seller's PAN for TDS deposit. Otherwise, deduct TDS at 20%.

- TDS is subtracted when paying (including instalments) the sellerThe TDS on the

- Form 26QB must be used to pay for immovable property within 30 days of the end of the month in which TDS was deducted.

- The buyer must give the seller the TDS certificate in form 16B after depositing TDS with the government. Approximately 10 to 15 days after the TDS deposit, this becomes available. Form 16B must be obtained by the buyer, who then gives it to the seller.

How to Pay TDS via Challan 26QB and Get Form 16

Follow these steps to pay TDS through Challan 26QB and obtain Form 16B:

Online e-Payment via Challan 26QB

Step-1:

Access your account on the Income Tax e-filing portal. select "e-Pay Tax" from the dropdown menu as displayed below.

Step-2:

Select '+ New Payment'

Step-3:

Click on the proceed button on the tab ‘26QB- TDS on Property’ as highlighted below

Note: Next, you will need to provide:

- Buyer's Details

- Seller's Details

- Property Details

- Payment Details

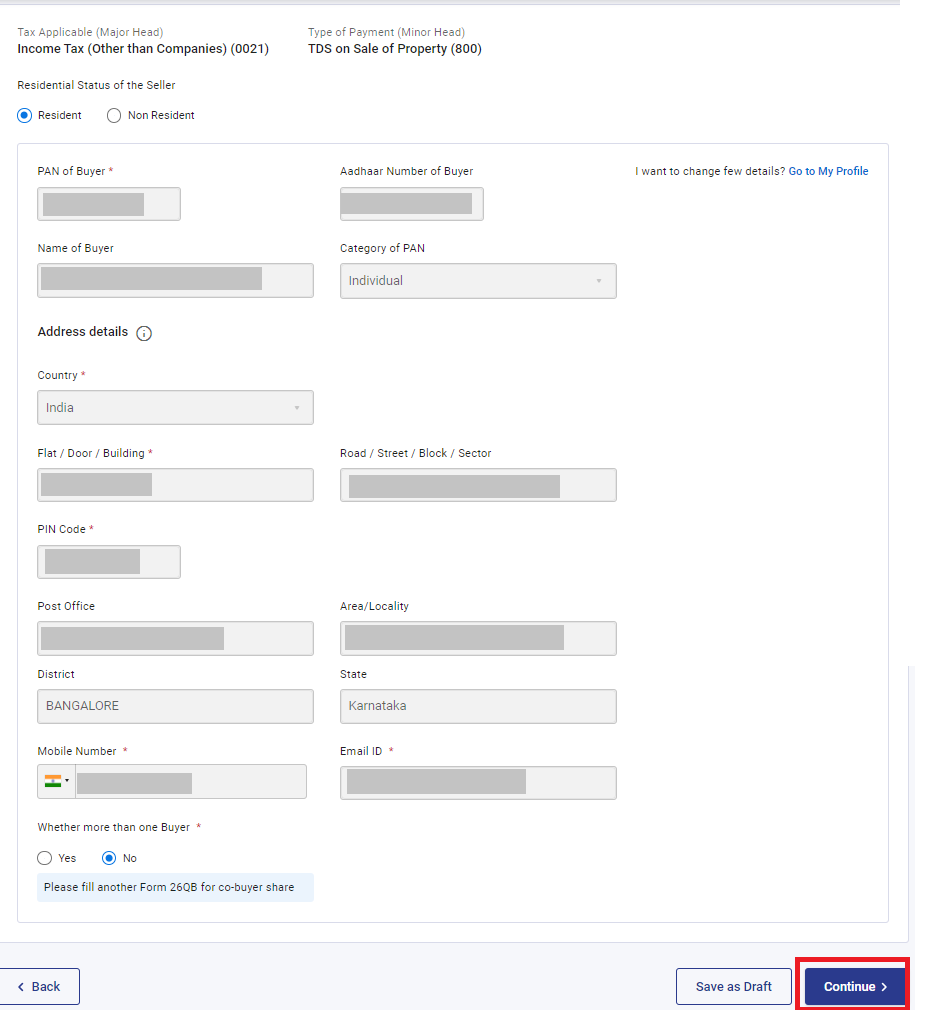

Step-4: Add Buyer's Details

Your details will be auto-filled, but can be updated. Click 'Continue' after entering details.

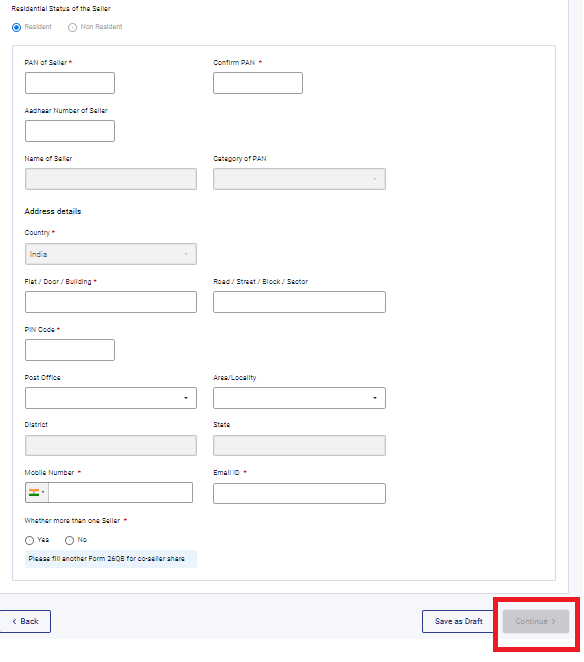

Step 5:

Add Seller's Details

Add all the details of the Seller like their PAN, address

Step 6:

Add Property Details

Input property and sale details such as type, address, agreement date, and value. The tax is calculated automatically. Click 'continue' when finished.

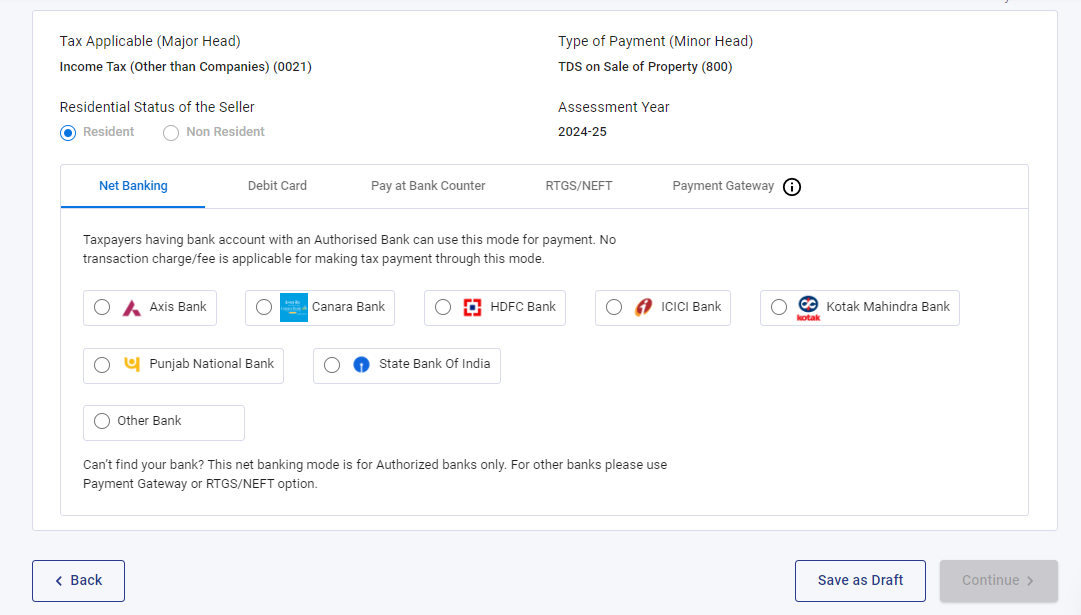

Step 7:

Add Payment Details

Choose a payment method and finish the transaction. A challan will be created after payment.

Step 8:

Register in TRACES

- Register on TRACES

- After registration, you can get approved Form 16B and issue it to the Seller.

- After seven days of payment, check your Form 26AS. You will notice that your payment is listed under "Details of Tax Deducted at Source on Sale of Immovable Property u/s 194(IA) [For Buyer of Property]".

- Part F details include TDS certificate number, deductee's name and PAN, transaction data, acknowledgement number from Form 26QB, deposit date, and TDS deposited.

Step 9:

Download Form 16B

- Once your Form 26AS payment is shown, log in to TRACES. Navigate to the Download tab and select “Form-16B (for the buyer)”.

- Complete the process by entering the seller's PAN and the property transaction acknowledgement number, then click "Proceed".

(1).png)

- Check details and click “Submit a request”.

.png)

- Your request will soon be processed. Go to the Downloads tab and select Requested Downloads.

.png)

- You ought to be able to see that your Form 16B download request has the status "available."

- Wait a few more hours if the status reads "submitted" before repeating the previous step.

- Get the ".zip file" now. The deductor's date of birth (in the format DDMMYYYY) serves as the password to open the ".zip file." Your form will be accessible as a pdf inside the.zip file. Please print this.

Form 26QB Non-filing Notice

The tax department gets regular property transaction reports. If a property transaction exceeds Rs.50 lakh and the buyer has not deducted 1% tax or not filed TDS on time, the department will send a notice to the buyer.

Taxpayer Notice Example

Subject: CPC (TDS)

Reminder: Pending 26QB Statement for Property Purchase in FY 2013-14

Communication Date: 05/04/2016

To: Property Buyer

PAN(XXXXX1234X)

According to the Annual Information Return (AIR), you purchased property over Rs.50 Lakhs in FY 2022-23. However, you haven't filed your TDS Statement in Form 26QB. Please urgently address this and issue the TDS Certificates in Form 16B from TRACES.

Form 26QB Filing Requirements

The Finance Act of 2013 mandates TDS on property transfers over Rs 50 Lakhs. Section 194 IA, along with Rule 30, 31 & 31A of the Income Tax Rules, provide the following directives:

- From June 1, 2013, a 1% tax must be deducted by the buyer at the time of payment.

- The deducted tax should be deposited to the Government Account via e-tax Payment or through authorised banks.

- The tax deducted under section 194-IA must be paid to the Central Government within seven days from the end of the month of deduction.

- The PAN of both seller and buyer must be provided in Form 26QB, available at www.tin-nsdl.com (http://www.tin-nsdl.com/).

- The buyer must issue a TDS certificate in Form 16B to the seller, confirming the tax deduction and deposit.

- Form 16B is downloadable after registering at www.tdscpc.gov.in (http://www.tdscpc.gov.in/).

Form 16B TDS Certificates from TRACES

- All buyers must issue TDS certificates from TRACES.

- You can visit the TDS Reconciliation Analysis and Correction Enabling System at www.tdscpc.gov.in.

- Only TDS Certificates from the TRACES Portal are valid.

Consequences of Non/Late TDS Statements Submission

For Property Buyer

- A fee under section 234E of the Act will be charged for not filing or late filing of Form 26QB.

- A daily fine of Rs. 200 will be imposed until the form is filed.

- The buyer may face penalties for late deduction, late payment and interest. Section 271H penalties may also apply.

For Property Seller

- If Form 26QB is not filed or filed late, TDS Credit claims cannot be made.

- The deducted tax must be deposited into the Government Account via e-tax payment option or any approved bank branches within seven days from the end of the month of deduction.

Penalties for Non-Filing of Form 26QB

|

Interest Due: |

Calculation |

|

Non-deduction of TDS |

1% per month from due date to actual deduction date. |

|

Non-deposit of TDS |

1.5% per month from deduction date to payment date. |

Late Filing Fee: |

Calculation |

|

Late filing fee under section 234E |

Rs 200 per day until Form 26QB submission. Buyer liable for late deduction and payment interest. |

Penalty: |

Calculation |

|

Penalty under section 271H |

Minimum Rs 10,000, maximum Rs 1 lakh. No penalty if TDS paid with late fee & interest, and statement submitted within 1 year. |

- Hotel Payments for Seminars

If hotels charge only for catering/meals and not for use of premises, only Sec.194C applies for the catering part.