F-14/15, Orbit Mall, Civil Lines, Jaipur-302006

F-14/15, Orbit Mall, Civil Lines, Jaipur-302006

Register & Login

Register & Login

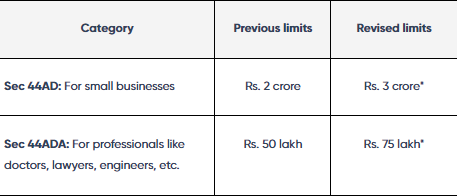

Budget 2023 Update

The 2023 Budget has ushered in some significant changes! One of these involves amendments to Sec 44AD and Sec 44ADA. These modifications have set new presumptive taxation limits for the Fiscal Year (FY) 2023-24, which will be applicable for the Assessment Year (AY) 2024-25. Here's the scoop:

The increase in limits is subject to a condition that the 95% of the receipts must be through online modes.

Section I: Businesses

Choosing the Right Legal Structure for Your Business

As you set off on your entrepreneurial journey, one of the first critical decisions you will need to make revovles around the legal structure of your business. The choice of your business's legal entity influences various facets such as taxation, liability, and compliance. Here are a few common legal entities you might consider:

- Sole Proprietorship

- Limited Liability Partnership

- Private Company

- Public Company

- Joint Venture

It's vital to remember that there's no legal requirement to structure your business as a 'company'. Incorporating a company certainly offers certain benefits, but it also involves additional compliance responsibilities. If your business is growing by leaps and bounds, to a point where it's becoming challenging to manage, splitting it into a separate legal entity might be a good idea. This new entity will have its own Permanent Account Number (PAN) and will file separate tax returns. On the other hand, if your operation is smaller or more manageable, you might opt for the simplicity of a sole proprietorship.

Let's Understand Bookkeeping Requirements

As a business owner, the income tax law obligates you to maintain books of accounts if you meet one of the following conditions:

a. Your income surpasses Rs. 1,20,000; or

b. Your total sales, turnover, or gross receipts exceed Rs. 10,00,000 in any of the three previous years.

The rules are slightly different for individuals and HUF (Hindu Undivided Family); you are bound by the requirement of maintaining books of accounts only when :

a. Your income overshoots Rs 2.5 lakhs or

b. Your total sales, turnover, or gross receipts are above Rs 25 lakhs in any of the three preceding years.

Keep in Mind:

Penalties related to non-adherence to bookkeeping:

If you haven't maintained the requisite book of accounts, it's important you know, the law may impose a penalty reaching up to Rs 25,000.

Getting Around Tax Audits

If your business sees gross receipts over Rs 1 crore in any fiscal year, brace yourself for a tax audit. Remember, the tax audit reporting due for filing stands at 30th September of the assessment year. This report should be filled out electronically using Form 3CD. In case a tax audit applies to you, the deadline to file your income return also is 30 September of the assessment year. Normally, you can't revise a tax audit report but if your accounts have been amended, a revision becomes possible.

Mark Your Calendar: Filing Deadlines

- Tax audit report due for filing: 30th September of the assessment year

- Income return filing due date (if subjected to tax audit): 30th September of the assessment year

- Income return filing due date (if tax audit is not required): 31st July of the assessment year

Deciphering Presumptive Taxation

Presumptive taxation clause can be located under section 44AD of the income tax act. Businesses with a turnover teetering below Rs 2 crore have the option to select presumptive taxation. These businesses must declare a profit of 8% for non-digital transactions or 6% for digital transactions - apply the one that fits your case. Don't forget, the below businesses are barred from this taxation model:

a. Life insurance agents.

b. Any form of commission-based businesses.

c. Businesses involved in leasing, hiring or plying goods carriages.

How to Calculate Presumptive Tax?

Let's run through an example:

Meet Lalit Traders: They earned gross receipts of Rs 1.5 crore for FY 2017-18 and decided against maintaining books of accounts. Having opted for presumptive taxation, they gathered Rs. 70 Lakhs through non-digital transactions and Rs. 80 Lakhs via digital transactions during the year. So, what would be the declared income under their business and profession head?

Your takeaway:

Let's break down the concept of income in business and profession sectors:

In non-digital transactions: 70,00,000 * 8% equals an impressive Rs. 5,60,000.

For digital transactions : 80,00,000 * 6% gets you a grand total of Rs. 4,80,000.

Your income under the category of “Business or Profession” will be a sum total of Rs 10,40,000 .

Enjoy the Perks of Presumptive Taxation

- Direct contributions to the National Defence Fund set up by the Central Government.

- Support the Prime Minister’s National Relief Fund.

- The presumptive taxation under Section 44AD sets your net income at 8% of your turnover, with tax being paid on this amount.

- If your income receipts are in digital (non-cash) form, only 6% of your receipts count as your net income and you will pay tax on this lower amount.

- No fuss about maintaining meticulous accounting records.

- No need to stress over getting your accounting records audited.

- You do need to pay advance tax – however, instead of constantly estimating income and paying tax every quarter, you can settle all your advance tax before March 31. Just keep in mind, if you've opted for the presumptive scheme, advance tax should be paid by 15th March of the relevant financial year if your income tax liability is likely to exceed Rs.10,000 in the financial year.

Discover International Transactions

When TDS is deducted by the foreign client

Let's say you provide services to clients overseas and you receive payments via PayPal, or as a direct credit to your bank account. Most often, the foreign client will withhold taxes in accordance with their local tax laws before releasing your payment. But don't forget, as an Indian resident, you're liable to Indian tax on all your income globally. However, you can claim credit for taxes paid in foreign countries in your income tax return.

What happens when TDS is not deducted by the foreign client?

In the situation where no TDS has been deducted by the foreign client, there's no need to hit the panic button. All you need to do is include these receipts in your total income for income calculations and pay the applicable tax, as you'll be a tax resident of India. In order to meet advance tax requirements, you may need to estimate your annual income from all sources.

Filing Your Return of Income

An individual or HUF running a business is legally obligated to file his return of income in form ITR 3. If you opt for presumptive taxation, your return should be filed using the very same ITR 3.

Section II: A Deep Dive into the World of Professionals

Professions Recognised Under Indian Tax Laws

- Engineering

- Legal practices

- Architectural pursuits

- Chartered Accountancy

- Medical practitioners

- Technical consultants

- Interior designers

Persisting Bookkeeping Practices

Maintaining Records for Specific Professions

If you're among the professionals performing the designated professions mentioned above, it's essential to maintain organized books of accounts in accordance with Rule 6F of the Income tax Rules. If your gross receipts exceed Rs. 1.5 lakhs during any three of the immediately preceding years, or even just on a single occasion in your professional startup year, it's time to maintain accounting records.

Here's a list of accounting records commonly prescribed under Rule 6F:

i. Cash Book – This straightforward record of your daily cash receipts and payments allows you to track your end-of-day or end-of-month cash balance.

ii. Journal – It's where you jot down your everyday transactions. All credits and debits must be recorded, especially if you follow the mercantile system of accounting.

iii. Ledger – This is the pool for all your journal entries, inclusive of all account specifics. It greatly simplifies your annual financial statement preparation.

iv. Always keep photocopies of all the bills or receipts valuing over Rs. 25.

v. And very importantly, keep the original bills or receipts for anything that costs more than Rs. 50. Additionally, if you are in the medical field, there are a few more records you should keep track of.

vi. Daily case registers that include patient details, received fees, provided services, and the date of receipt.

vii. Keep up-to-date stock information about medicines and other consumables.

Maintaining Records for Unspecified Professions

If your profession isn't mentioned above, you still need to maintain relevant books of accounts. These records should allow an assessing officer to calculate your taxable income in accordance with Income tax laws. This requirement comes into play when an individual’s income exceeds Rs. 2.5 lakhs or gross receipts are more than Rs. 25 lakhs in any of the three immediately preceding years.

Calculating Taxable Income

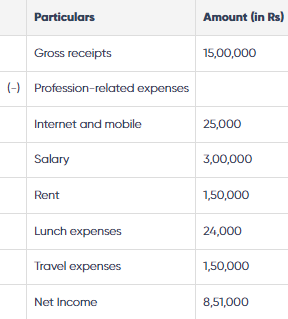

As a professional, you can quickly ascertain your taxable “Income under the head Profits and Gains from Business or Profession”. How? Simply subtract all profession-related expenses from your gross receipts. These expenses might include salaries, rent, internet and mobile expenses, official travel, and lunch expenses connected with your professional duties.

Let's consider a scenario:

Meet Archana. She's an interior designer and has recorded gross professional revenue of Rs 15 lakhs for the fiscal year 2017-18. Her expenses include:

- Internet and mobile – Rs 25,000

- Salaries for her two staff members – Rs 3 lakhs

- Rent for her workspace – Rs 1.5 lakhs

- Lunch expenses – Rs 24,000

- Travel expenses – Rs 1.5 lakhs

Now, let's see how we can calculate her taxable income from her profession:

Archana's income will sum together with her other taxable income. Her taxes are then calculated based on the applicable tax slab dictated by the total sum of her earnings. Essentially, what she owes in taxes directly correlates to her total income.

Filing Your Taxes

As a professional, your applicable form is ITR 3. Remember, your tax returns file should be ready on or before the 31st of July of the Assessment Year. This is, of course, unless you're subject to an audit under the Income-tax Act.

Who Needs a Tax Audit?

Did you know, if your gross professional revenue surpasses Rs 25 lakhs in a financial year, you are liable for a tax audit? Make sure to get your books audited, or you could face a penalty. This penalty could be as much as 0.5% of your gross revenue or Rs 1.5 lakhs, whichever is lower.

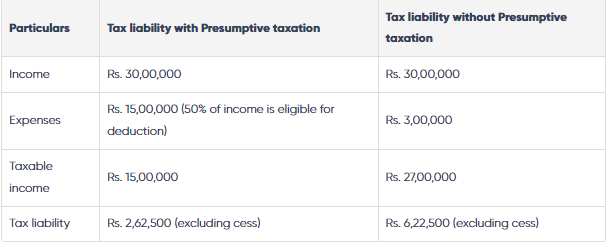

The Ins and Outs of Presumptive Taxation

If you're a professional with a gross revenue of up to Rs 50 lakhs, may we introduce you to the presumptive tax scheme. This scheme allows you to offer 50% of your gross revenue as your taxable income, and taxes are then levied on that income based on your slab rates. However, once you opt-in to this scheme, you no longer can claim professional-related expenses as a deduction.

What's more, if you choose this scheme, you won't have to maintain books of accounts. Even though you'll still have to file your return by the 31st of July of the assessment year, you should do so using ITR 4.

Moreover, you'll be liable for a tax audit if your declared earnings are less than a presumptively computed income and your earnings cross the basic exemption limit.

To better understand when it's advantageous to opt for this scheme, let's consider the following example:

Example:

Meet Rakesh. He's a practicing doctor with an annual income of Rs 30 Lakhs for the 2017-18 financial year. Running his practice incurs Rs 3,00,000 in expenses each year. Let's examine Rakesh's tax liability for FY 2017-18:

Simply by adopting the system of presumptive taxation, Rakesh can secure a sizeable saving of Rs. 3,60,000 in tax liabilities. Isn't that quite a relief for him?

Income Streams for Freelancers

If you're a freelancer engaged in any specific or non-specific profession, the tax rules that apply to you are no different than those for full-time professionals. This means taxation rules cover earnings, tax responsibility, record-keeping, presumptive tax regime, and all aspects related to your tax return filing.

Section III: Catching the Other Rules

Decoding Tax Jargon

Navigating the complex maze of Indian income tax laws can be quite intimidating. So, let's save you some precious time and confusion by explaining some essential tax terminologies that'll simplify your tax filing process.

The Business Diary: Books of Accounts

Imagine your business diary, 'Books of Accounts,' showcasing a clear snapshot of your income, expenses, assets, and liabilities. It is an indispensable tool when it comes to understanding your business performance and is usually a compulsory requirement in certain scenarios.

Your Safeguard: Deductions

Picture your total earnings or gross income as a big cake. Now, from this cake, you can claim 'deductions.' They are like slices of cake you get to keep, reducing your taxable income and hence, your tax liability. These deductions could be tax-saving investments like PPF, NSC, or expenses like life insurance premiums, interest on education loans, medical insurance premiums, and more.

Your Asset’s Lifeline: Depreciation

When you buy a capital asset like machinery for your business, it’s not a one-time expense but an investment expected to serve you for years. So, a portion of its cost is acknowledged as an expense each year, reducing your taxable income, which is known as 'depreciation.'

The Withheld Amount: Tax Deduction at Source (TDS)

In the world of taxes, TDS is like an advance payment collected by the tax authorities. If someone owes you money, they're required to deduct a portion as tax before paying you the rest. You then account for the gross amount while filing your returns, adjusting the TDS against your final tax liability. This way, the government ensures a steady inflow of taxes.

Your Tax Installments: Advance Tax

With the system of 'Advance Tax,' it's more of a pay-as-you-go approach than a big-fat tax bill at the end of the year. These tax payments are made in installments, guided by specific due dates set by the income tax department.

Your Tax Report Card: Form 26AS

Consider Form 26AS as your financial yearbook containing all the tax-related information linked to your PAN. It covers TDS, taxes you've deposited, refunds you've received, and more. To check out your tax report card, all you have to do is access and download your Form 26AS here.

Your Fiscal Checkup: Tax Audit

A tax audit is your accountant's version of a yearly health checkup where a Chartered Accountant reviews your financial records. If you're a:

a. Professional earning above Rs. 50 lakhs,

b. Business owner with an annual revenue exceeding Rs.1 crore or

c. Have opted for presumptive taxation but your total income surpasses the basic exemption limit of Rs. 250,000 and you declare your income below the stipulated percentage;

Your financial records have to go through this checkup or 'audit.'

Your Digital Proof: Digital Signature

When you file your audit report, a digital imprint of your assent is needed- the 'Digital Signature.' These come with a validity of one or two years, and both the Chartered Accountant and you must sign digitally.

Your Tax Snag: Defective Return Notice under 139(9) for Freelancers

Sometimes, hiccups happen. Like, when you file an income tax return using ITR-3 Form, and somehow, fail to provide complete details in the Profit & Loss and Balance Sheet sections, your return might be handled as defective under Section 139(9).

Your Expense Guide: List of Deductible and Non-deductible Expenses

- Office rent whether for individual or shared space

- Professional meals and travel expenses

- Costs linked to advertising, promotions, and prints

- Depreciation on equipments like laptops or computers. View the official depreciation rates given by the Income Tax Department

- Private platform fees for filing Income tax return like ClearTax

- Travel expenditures related to your profession

- Conveyance expenses

Frequently Asked Questions

When should an individual in business or a profession file their income tax return?

If you're running a business or practicing a profession, you're required to file your income tax return by July 31st of the assessment year. In case you're subject to a tax audit, you have the flexibility to file your return anytime up until September 30th of the same assessment year. Keep in mind though, if the Central Board of Direct Taxes (CBDT) announces an extension, these due dates can shift.

What is the due date for filing of return of income by an individual carrying out a business or a profession?

As a businessperson, you would be subject to an audit under Section 44AB of the Income-tax Act if your total business turnover exceeds Rs 1 crore. If you're a professional and your gross receipts go beyond Rs 25 lakhs, then you too would be liable for a tax audit.

When will a businessman or a professional be subject to tax audit?

Yes, you absolutely should. If your business turnover goes above Rs 25 lakhs in any of the immediate 3 preceding years, it is mandatory for you to maintain your books of accounts. Failing to do so can land you with a penalty of Rs 25,000.

I run a small business with a turnover of about 30 lakhs on an average every year. Do I have to maintain accounting records?

With the presumptive scheme of tax, you're typically exempt from quarterly advance tax payments. However, you are required to get all your advance taxes paid by March 15th of the relevant financial year. And any taxes paid before March 31 will be considered as advance taxes.

I have opted for the presumptive scheme of tax. Should I still pay advance tax?

No, when you declare the prescribed proportion of your gross receipts or turnover as income under the presumptive scheme, you're not allowed to claim any further expenses as a deduction.

Can a person opting for presumptive scheme of tax claim any further expenses from his gross income?

No, there's no need for you to maintain any books of accounts if you've opted for the presumptive income scheme under Section 44AD, 44ADA, 44AE etc. It's one less thing for you to worry about!

Should a person offering income presumptively maintain books of accounts?

Once you're in, you're committed to ride it out for 5 years. If you opt out in any of the 5 years, you won't be eligible to opt back in for the next 5 years. For instance, if you claimed to be taxed on a presumptive basis under Section 44AD for AY 2016-17, followed it up for 17-18, and 18-19, but bailed out for AY 2019-20, you won't be able to avail the benefits of the scheme for the next five assessment years, that is from AY 2020-21 to 2024-25.