F-14/15, Orbit Mall, Civil Lines, Jaipur-302006

F-14/15, Orbit Mall, Civil Lines, Jaipur-302006

Register & Login

Register & Login

Hey there! Did you know that the taxes we pay as citizens serve as the bedrock of the Indian economy? Pretty important, right? Now, if you happen to be earning an income from afar, don't worry, you're not left out. The Indian Income Tax Act of 1961 has a special provision, NRI taxation, just for those making money beyond India's borders. The catch is, the tax rules and benefits for NRIs are quite distinct from those for resident Indians. Fascinating, isn't it?

How do I determine my residential status?

Are you unsure of your tax residency status for the financial year? Don't fret, it's simpler than you think! Based on Indian tax laws, here's how you'll recognize if you're considered an Indian resident for the financial year. If any of the conditions listed below apply to you, then congratulations! You meet the requirements.

- Enjoying your time in India? If you've been exploring the vibrant culture of this country for at least half the year (yes, we're talking about 182 days), during a financial year, did you know that it could impact your taxes? Also, if you've spent a shorter stay of about 2 months (or 60 days) in the previous year, but you've got a total of one full year (that's 365 days) under your belt in the past four years, you'll find this information handy as well.

Note: If you are an Indian citizen working abroad or a crew member on an Indian ship, only the first condition is available to you – which means you are a resident when you spend at least 182 days in India.

Let's talk about folks known as a Person of Indian Origin (PIO) who are visiting India. The rule of thumb doesn't quite apply to them as it would ordinarily. A PIO is someone whose parents or even grandparents were born in the territories of undivided India. Fascinating, isn't it?

If you find that you don't fit any of the above labels, my friend, you ought to identify as a Non-Resident Indian.

Onto the revised definition of a Resident but Not-Ordinary Resident (RNOR),

You're deemed an RNOR for the year if you can check off any of these boxes:

- Being a non-resident in India for 9 years out of the last 10 years, or

- Hanging out in India for 729 days or less over the last 7 years.

Through the Finance Act 2020, the rules have been tweaked a bit more. Indian Citizens/Persons of Indian Origin visiting India now might be considered RNORs if they fulfill certain criteria:

- Income from sources other than foreign ones totals Rs 15 lakh or more

- Time spent in India ranges from over 120 days to under 182 days in the last year

- The person has stayed in India for 365 days or more over the past four years

Prior to these changes, individuals like these would be classified as non-residents. Now they may find themselves under the RNOR category, which might result in losing their DTAA benefits, an expanded scope of their total income subject to taxation, and the loss of various exemptions. Just something to be aware of!

Note that, regardless of their income in the previous year, an individual spending more than 182 days in India will be recognized as a resident in light of the latest amendment.

Another new term thanks to Finance Act 2020 - Deemed residency

Under this Act, ‘Deemed residency’ was coined. Simply explained, Indians earning more than Rs 15 lakh from Indian sources, but aren't taxed elsewhere, will be considered residents of India.

So, these deemed residents, effective since the financial year 2020-21, will be classified as RNORs. This amendment was enacted to ensure tax compliance for Indian citizens who don't pay tax in any other country.

Here's something specifically relief due to the COVID lockdown

For the FY 2019-20, if you came to India before 22nd March 2020 and found yourself:

Is my income earned abroad taxable?

If you're an NRI, your income tax obligations in India hinge on your residential status for the year - based on the applicable income tax regulations.

Now, you might be wondering, what does this mean exactly? Well, if your status is classified as ‘resident,’ then brace yourself because your global income is taxable in India. If, however, your status is ‘NRI,’ only the income you make within India is taxable here.

- Let's understand this better with some examples. Suppose you receive a salary in India or for services provided in India, own a property that generates income, or make some neat gains from transfer of assets based within India, all these forms of income are taxable for an NRI. Even income from fixed deposits or the interest earned on a savings bank account fall in this bracket.

- However, if you're earning a buck or two outside India, rest easy! This income isn’t taxable under the Indian revenue system.

- Any interest that accrues on your NRE (Non-Residential External) account or a FCNR (Foreign Currency Non-Resident) account is tax-free. But remember, the interest accumulated on NRO (Non-Resident Ordinary) accounts is taxable in the hands of an NRI.

Am I required to file my income tax return in India?

NRI or not, any individual whose income exceeds Rs 2,50,000 is required to file an income tax return in India.

Let's Dive into a Real-Life Scenario:

Meet Srishti, an Indian living and working in the United States. While checking her Form 26AS online, she notices a TDS entry for Rs 20,000. It seems this TDS was held back at a 30% rate on the interest she earned from her NRO account. Now she's left wondering if she's obligated to pay any more tax in India, or even, to file an income tax return? Let's delve into her situation.

Whether or not you have to pay tax in India really depends on your residential status. So, our first step is to figure out Srishti's status.

Srishti is an Indian citizen who took up employment in the U.S. To be considered a resident in India for tax purposes, she'd need to spend 182 days or more within its borders.

Consider this: Srishti left India on July 3, 2020, and returned on March 15, 2021. Given the financial year beginning April 1, 2020, and ending March 31, 2021, we can see that Srishti stayed less than 182 days in India. As such, according to Indian tax laws, she is classified as a Non-Resident Indian (NRI).

Here's the catch for Srishti: Only the income she earns or accrues in India will be taxable. Her U.S. income? Not taxable in India because she's an NRI. It's also worth noting that interest earned on an NRO account is taxable for an NRI, but NRE account interest earnings are tax-free.

What's next? Srishti needs to calculate all her income originating in India. With Rs 70,000 earned as interest on her NRO account standing as her only income, what is her tax liability?

For FY 2020-21, any income under Rs 2.5 lakh is exempt from tax. Since Srishti's total income falls below this threshold, she owes no additional tax. However, since tax was already deducted from her interest income, she should file for a TDS refund.

Remember, claiming a refund can only be done by filing an income tax return for the corresponding financial year.

When is the last date to file an income tax return in India?

July 31st is the last date to file income tax returns in India for NRIs unless the government extends it.

Are NRIs required to pay advance tax?

Wondering whether NRIs have to shell out advance tax? Well, if an NRI's tax liability exceeds Rs 10,000 in a financial year, they're definitely on the hook to pay it. And don’t forget, if you overlook paying your advance tax, you’ll be hitting up against interest as per both Section 234B and Section 234C.

What counts as taxable income for an NRI?

When it comes to salary income, if you're an NRI, it's the place of receipt that matters. That is, if you receive your salary in India or if someone receives it on your behalf there, then brace up! It's going to be taxed according to Indian laws. Your slab level in the tax structure will shed light on exactly how much you owe.

What about income from salary?

Here's the thing - your income from salary will come under the Indian tax scanner if your services are being offered in India.

This means that even if you're an NRI, if the work you're doing is in India, it's going to be taxed in India, regardless of where you're actually pocketing the income.

Are you an Indian citizen working for the Government of India outside of the country? Well, then your income from this service, even if delivered abroad, is taxable back home.

However, Diplomats and Ambassadors, you can breathe a sigh of relief - your income's off the tax grid. Take Ajay's example. He worked on a project in China for an Indian company for 3 years. He preferred receiving the salary in India to manage his family's needs and home loan payments. But, mindful of the Indian tax liabilities, he decided to receive it in China instead.

Income from house property

Income from a property that is situated in India is taxable in the hands of an NRI.

The calculation of such income shall be in the same manner as applicable to a resident. This property may be rented out or lying vacant. An NRI can claim a standard deduction of 30%, deduct property taxes, and benefit from an interest deduction from a home loan. The NRI is also allowed a deduction for principal repayment under Section 80C. Stamp duty and registration charges paid on purchasing a property can also be claimed under Section 80C.

Income from house property is taxed at slab rates as applicable.

For instance, Nandini owns a house property in Goa and has rented it out while she lives in Bangkok. She has set up the rent payments to be received directly in her bank account in Bangkok. Nandini’s income from this house which is located in India, shall be taxable in India.

Rental payments to an NRI

A tenant who pays rent to an NRI owner must remember to deduct TDS at 30% while paying rent.

The income can be received to an account in India or the NRI’s account in the country they are currently residing in.

For instance, Maria pays a monthly rent of Rs 30,000 to her NRI landlord. She must deduct 30% TDS or Rs 9,000 before transferring the money to the landlord’s account.

Picture this: Maria is paying a monthly rent of Rs 30,000 to her landlord, who happens to be a Non-Resident Indian. Sounds straightforward, right? Not quite. Before Maria sends her rent payment, she's required to deduct a hefty 30%, or Rs 9,000, as TDS. This chunk goes right off the top before she transfers the cash into her landlord's account.

It doesn't end there for Maria. Next, she has to tackle Form 15CA and submit it online to the big guns at the income tax department. This is a mandatory step for anyone making a payment to a Non-Resident Indian like Maria's landlord. And did we mention this form has to be submitted online? Yes, it sure does. In certain cases, Maria would also need to garner a certificate from a trusty chartered accountant in Form 15CB before she could even think about uploading Form 15CA. In this Form 15CB, a chartered accountant validates information ranging from the specifics of the payment, the TDS rate, and TDS deduction according to Section 195 of the Income Tax Act, to whether any Double Tax Avoidance Agreement (DTAA) applies, and even the other nitty-gritty details about the nature and purpose of this remittance. A mouthful, right? But no need to worry, Maria's got it down pat.

- Should your remittance not go beyond Rs 5,00,000 (all together in a financial year), you'll just need to submit Form 15CA. Easy peasy.

- Now, suppose you've received a certificate under Section 197 because lower TDS needs to be taken out. In that case, the AO demands that lower TDS be deducted – as simple as that.

- And guess what, my friends? If the transaction is under Rule 37BB of the Income Tax Act, featuring 28 items, you don’t need either of these! Take a quick look at the whole list right here by clicking this link.

- In all other situations where you want to make a remittance outside India, don't sweat it. Just get a CA’s certificate in Form 15CB. Once it’s in your hands, take a moment to submit Form 15CA to the government online. Done and dusted.

Discover the World of "Income from Other Sources"

Current holder of a fixed deposit or savings account in an Indian bank? Then you're not exactly tax-free. The interest income you're receiving is taxable in India. Now, details may differ based on the type of account. For instance, take note - Interest accrued on NRE and FCNR accounts are tax-free. But the catch? NRO accounts bear full tax liability.

Expanding on "Income from Business and Profession"

Are you a Non-Resident Indian (NRI) with a business in India? Then be aware! Any income generated from a business you control or have established in India will be subject to tax.

Gains & Losses: "Income from Capital Gains"

Transferring a capital asset located in India? That's a taxable act right there. Capital gains arising from the transfer of such assets are subject to tax in India.

Even income derived from investments such as Indian shares and securities falls under the tax radar in India. So, let's say you sell a house property, which results in a long-term capital gain. In this scenario, the buyer is obligated to deduct TDS at 20%. Don't fret, you still have an escape hatch. Avail of the capital gains exemption by investing in either a house property in accordance with Section 54, or capital gain bonds aligned with Section 54EC.

All About Special Provision for Investment Income

Are you an NRI who's invested in Indian assets? Then you should know that you'll be taxed at 20% on your income! But there's some good news. If your only income in a financial year is from this investment and your TDS has already been deducted, you're off the hook for filing an income tax return.

Is Your Investment Eligible for Special Treatment?

Curious to know which investments get this special perk? Here's a list of assets, all to be acquired in foreign currency, which make you eligible:

- Own any company shares, whether public or private, in India

- Have debentures in a publicly-listed Indian company – avoid private ones for this purpose, though

- Place deposits with banks or public firms

- Hold securities of the Central Government

- Own other central government assets that make the cut according to the official gazette.

- Tough luck, though! Any deduction under Section 80 won't be considered when calculating your investment income.

A Closer Look at Special Provision for Long-Term Capital Gains

If you've made some long-term capital gains by selling or transferring your foreign assets, you should keep in mind that there's no slimming down of the gains through indexation, nor can deductions be claimed under section 80.

However, if you're looking to reinvest these profits, then you can qualify for an exemption under Section 115F by channeling your profit back into: - Shares of any Indian business

- Debentures of an Indian publicly-run company

- Deposits with Indian banks and public firms

- Securities of the Central Government

- NSC VI and VII issues

If your reinvestment is less than the profit you made, enjoy a proportionate tax break as per the new asset's cost.

Don’t forget! If you decide to sell or transfer this new asset within three years of acquisition, you'll lose your exemption. That profit will rejoin your taxable income in the year of sale/transfer.

And the cherry on top? These benefits are still within arm's reach even if you change your NRI status – as long as that asset hasn't been turned into cash. However, a declaration by you to the assessing officer stating your intention to apply these special provisions is expected.

If you think the special provisions are too tricky to handle, you can willingly opt out. In that case, your income from investments and long-term capital gains (LTCG) will follow the general rules stated in the Income Tax Act.

- Need a tax whiz to help you with your IT returns?

Look no further! Allow us to assist you with your income tax and filing needs. Our experts can whip up your tax return and e-file it within just 48 hours. Rates start from Rs 3,100 for Non-Resident Indians (NRIs).

Enlist an Expert

Let's talk NRI deductions and exemptions!

Like resident Indians, NRIs can also pocket various deductions and exemptions from their total earnings. Let's dive into some of them:

Section 80C Deductions

The majority of deductions under Section 80C are available for NRIs just like for residents. For FY 2020-21, an individual can cut down the gross total income up to Rs 1.5 lakh with deductions allowed under Section 80C.

Here are the 80C deductions NRIs can claim:

i.Life insurance premium payment: You can claim this deduction if the policy is in your name, your spouse's, or any of your children's names (dependent/independent, minor/major, or married/unmarried). Just remember, the premium must not exceed 10% of the sum assured.

ii. Children’s tuition fee payment: Paying tuition fees for any two children studying at any school, college, university or other educational institution located within India could earn you a deduction. This includes fees for play school, pre-nursery, and nursery education as well.

iii. Principal repayments on a home loan: If you have taken a loan to buy or build a residential property, the principal repayment could qualify for a deduction. You may also claim the stamp duty, registration fees, and other expenses related to the property transfer.

iv. Unit-Linked Insurance Plan (ULIP): A ULIP, which combines life insurance protection with investment, is also eligible for a deduction under Section 80C. This includes contributions to LIC mutual fund unit-linked insurance plans like Dhanraksha 1989 and others offered by UTI.

v.Investments in ELSS: ELSS has been a hot favorite lately since it allows deduction under Section 80C up to Rs 1.5 lakh. Plus, it offers a triple E (Exempt-Exempt-Exempt) benefit to taxpayers, and it's a great way to earn as these funds primarily invest in a diversified equity market.

Digging Deeper: Additional Deductions

Hey there! Just a heads up, as an NRI, you've got a few more deductions to claim apart from those under Section 80C. Let's dig deeper into these:

Claiming Deductions from House Property Income made Easy

Here's some good news! As an NRI, you can enjoy the same deductions as a resident Indian including insurance deductions from income from property purchased in India. Even the property tax paid and interest on your home loan is deductible. Want more info? Dive into the world of house property income

Shave off Some More with Section 80D

If you're shelling out funds for health insurance, there's a deduction waiting for you! This one, available up to Rs 25,000, covers you, your spouse, and your dependent children. What's more, you can also claim up to Rs 25,000 for insuring your parents.

Senior citizens, listen up! The deduction limit hikes up to Rs 50,000 if the insurance premium caters to resident senior citizens. little hiccup here, this does not cover insurance premiums paid for senior citizen NRIs under Section 80D.

Did you know you can get a deduction of up to Rs 5,000 for preventive health check-ups? Plus, if you incur medical expenses up to Rs 50,000 for resident senior citizens, that can also be claimed within the existing limits of Section 80D. Just ensure they aren't otherwise covered under a health insurance policy.

Section 80E: Snag a Deduction on Education Loan Interest

Got an education loan for higher studies? NRIs, you can claim a deduction on that interest. And yes, even if the loan is for your spouse, children, or a student you have guardianship for. There's no cap on this deduction and you can claim it for a maximum of eight years or till the interest is paid off, whichever comes first. Note: the principal repayment doesn't get the deduction benefit.

Social Causes and Section 80G Deductions

Charitable at heart? Your donations can help you claim a deduction under Section 80G. Curious about what goes into this? Check it out and find out.

Section 80TTA: Deductions on Savings Account Interests

NRIs, enjoy similar privileges as resident Indians and claim a deduction on savings bank account interests. The cap is Rs 10,000 on deposits in savings accounts (not time deposits) with a bank, co-operative society, or post office starting FY 2012-13.

NRI Deductions: What Doesn't Make The Cut?

Some Section 80C Investments:

- New PPF account investments are a no-go for NRIs, though existing ones can be maintained

- National Savings Certificates (NSCs) investments

- Post office 5-year deposit scheme

- Senior Citizen Savings Scheme (SCSS)

Section 80DD: Deduction for Differently-Abled Not Available for NRIs

The deduction under Section 80DD includes expenses for medical treatment and maintenance of a differently-abled dependent. Unfortunately, this one doesn't extend to NRIs.

Section 80DDB: NRIs Not Eligible for Differently-Abled Deductions

Under Section 80DDB, a deduction for medical treatment of a disabled dependent is reserved only for residents.

No Section 80U Deduction for Differently-Abled NRIs

This one applies to disability cases where the taxpayer is disabled themselves. However, it's only available to resident Indians.

NRI and Property Sales: Exemptions Uncovered

Did you know that long-term capital gains are slapped with a 20% tax? And if you're an NRI, this also entails a TDS of 20%. But don't be daunted just yet!

As an NRI, you too can claim exemptions under Section 54, Section 54EC, and Section 54F for long-term capital gains. So, the next time you file a return, don't forget to claim a refund of the TDS deducted from your Capital Gains.

Here's a little heads up: exemption under Section 54 permits long-term capital gains on the sale of a house property; whereas Section 54F lays down exemptions 2 on the sale of assets other than a house property. Still, puzzled about Section 54? Here's everything you need to know.

Section 54EC too aids in exemption, especially when capital gains from the first property sale are reinvested into specific bonds.

- Now, let's say you're not too thrilled about reinvesting your profit from the first property sale into another. In that case, you can safely park them in bonds for up to Rs 50 lakh issued by NHAI or REC.

- You have a period of 6 months to invest the profit in these bonds, but remember, to claim the exemption, the investment should be made before the tax filing deadline.

- The invested money can be withdrawn after 3 years but selling them before 5 years from the date of sale is not permitted. FYI, from FY 2018-2019, the period of 3 years has been pushed to 5 years.

- From FY 2018-19, exemption under Section 54EC has been confined to capital gain arising from the transfer of long-term capital assets being land and building or both. Previously, this exemption was accessible on the transfer of any capital assets. NRIs need to make these investments and show valid proof to the buyer to avoid TDS being deducted from the capital gains. They can also claim a refund of the excess TDS deducted at the time of return.

How do different situations affect your tax?

Temporarily working abroad

Take the case of Rahul, who worked out of Singapore for 4 months and earned in Singaporean Dollars during that time. He got this income credited to an Indian bank account. Now, he's back home. So, how should he file his income tax return?

Rahul’s taxes for this year hinge upon his residential status. As Rahul hasn't been outside India for more than 182 days, he'll be considered a resident. Hence, he needs to file his income taxes in India this year, that too including his Singapore stint's salary. However, if the assignment stretches beyond 182 days, Rahul’s residential status will transform, and he’ll be obliged to pay taxes only on the Indian income earned so far. Remember, Rahul’s foreign income credited to an Indian bank account is chargeable in India.

Recently relocated overseas

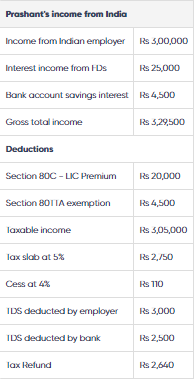

Let's take Prashant’s scenario. He recently moved to the US for a new assignment. His US income gets credited to an NRE account in India. He still invests in FDs and has some money in a savings account in India. He just received Form 16 from his Indian employer. So, should he file an Indian tax return this year?

Whether an NRI or not, every individual earning more than Rs 2,50,000 must file a tax return. However, keep in mind, NRIs are only taxed for income earned/collected in India. So, Prashant will be liable to pay taxes on Indian income and earnings from FDs and savings accounts.

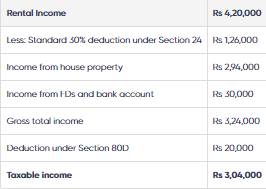

The Adventure of International Living

Picture this; it has been a full three years since Arjun courageously embarked on his new adventure, moving from India to the US. Now earning in crisp US dollars, he hasn't let distance sever his financial ties to his homeland. Arjun keeps some of his wealth simmering in an Indian savings account and Fixed Deposits. Besides these, he made a savvy investment by purchasing an apartment in India, which now brings in a sweet monthly rent of Rs 35,000. But that's not all! As a doting son, he gifted his parents a shiny new car and makes a monthly transfer of Rs 10,000 to support their household. He also funnels Rs 20,000 into his father's account annually to cover the insurance policy he secured for his beloved parents.

Did you know that Arjun's monetary gifts to his parents are tax-free? Just like that, Rahul can make the most out of Section 80D by claiming a tax deduction of Rs 20,000 on insurance expenses for his parents. However, since Rahul's gross income surpasses the Rs 2,50,000 limit, he must file an income tax return in India.

A Warm Welcome Back to India For NRIs

Let's switch gears and speak about our recently returned NRIs, who are now referred to as RNORs (Resident but Non-Ordinary Residents). Here's the lowdown on when you become an RNOR:

- If you've been an NRI for nine out of the last ten fiscal years

- If your stay in India for the past seven years has been 729 days or less

Now, here's some good news - the Indian IT Department likes to make your transition back home smoother. How? Well, you'll continue to enjoy the tax exemptions that you once had as an NRI for two more years after your return! Therefore, any deposits in foreign currency that were tax-exempt as an NRI continue to be so for the next two years. Afterwards, however, returning NRIs will be treated as normal residents.

Calling All Indian Residents with Global Income!

Here's a quick head's up for you global butterflies out there: if you're an Indian resident, your income from any corner of the world is taxable in India. Don't worry, though - If the global income is subjected to tax in another country besides India, take advantage of the DTAA (Double Tax Avoidance Agreement).

Let's Dive Into a Practical Case:

Shreya made her way back to India in 2010, after a five-year stint in London. Despite being miles away, her French employer retained her and still sends her consultation fees in pounds. As she pays the tax there, does Shreya need to include this in her income tax return in India?

As an Indian resident, Shreya's income from across the globe, even the consultant fees in pounds, is taxable in our country. Her pounds income will be converted to Indian rupees for tax calculations and merged with her total income, taxed as per official slab rates.

A silver lining here is the DTAA. If Shreya has already paid tax on her income in the UK, she can claim benefits under DTAA and save herself from double taxation, thanks to the provisions between the two countries.

If you're a resident with global income streaming in, remember to include it in your income tax return.

Decoding Income Tax for Expatriates in India

If you're a foreign national living in India, you might be wondering about your tax obligations. Well, let's cut through the jargon, shall we?

Get the lowdown on how expatriates in India can manage their income tax returns right here.

Navigating Double Taxation as a Non-Resident Indian (NRI)

Are you an NRI worried about paying taxes twice on the same income? Fear not, friend, there's a handy tool at your disposal known as the Double Taxation Avoidance Agreement (DTAA).

Through the DTAA, there are two pathways you can take to avoid the brunt of double taxation - the exemption method and the tax credit method. The exemption method gives you a tax break in one of the two countries. The tax credit method, on the other hand, provides a tax relief benefit in your country of residence, even if the income has been taxed in both countries.

And there's even more good news! The Budget 2021 has brought forth a new provision - Section 89A. This section aims to alleviate the undue taxation burden on NRIs (specifically, those with foreign retirement accounts), by focusing on the phase of tax - on accrual or withdrawal.

Your Burning Questions Answered

What qualifies as being a non-resident Indian (NRI)?

Let's put it simply. If you're not residing in India, you're an NRI. Some rules apply here though. You're deemed a resident if you spend 182 days or more in India during the financial year, or if you've been in India for 60 days or more in the current year and for 365 or more days during the previous four years. If neither of these conditions applies to you, congratulations, you're an NRI!

Do I, as an NRI, need to pay taxes in India on my US salary?

Good news! As an NRI, you only need to shell out taxes on the income you generate within India. So, your US salary? Not taxable here! You will, however, need to pay taxes on any rental income earned from a property in India.

When should I, an NRI, file my income tax return in India?

NRIs are pretty much in the same boat as resident taxpayers in this regard. If your total income earned in India crosses the Rs 2.5 lakh threshold in a financial year, it's time to file your returns. And remember, you better be punctual! Tax filing is usually due by July 31st of the assessment year, barring any official extensions.

I'm a 65-year-old NRI. Am I exempt from filing returns if my income from India is Rs 2.8 lakhs?

Sorry, friend. The Rs 3 lakh and Rs 5 lakh exemptions are only available for resident senior and super senior citizens. So, even if you are a senior citizen, as an NRI, any income exceeding Rs 2.5 lakh requires you to file your returns in India.

Do payments to NRIs come with tax deductions?

Bingo! Payments like rent, and professional or technical fees made to an NRI do require tax deduction at source. Those making payments need a TAN to deduct taxes and adhere to certain forms for compliance. Dive deep into the subject with our guide on Form 15CA and 15CB.

Will I, an NRI, need to pay taxes in my home country on the income I earn in India? How can DTAA help me?

If as an NRI, you earn income in India, that income is indeed taxable right here. It might also be taxed by the country where you're a resident. It sounds unfair, right? That's precisely where DTAA comes to the rescue. It helps you avoid the burden of double taxation by allowing you to claim credit for the taxes you've paid abroad while filing your taxes home.

As an NRI, if I sell a property in India, will it incur capital gains tax?

Yes indeed, my friend, it will. Selling the flat you own in India will mean you're liable to shell out capital gains tax. The amount of tax owed depends on both, the gain you make from the sale and the type of asset. The buyer is usually responsible for deducting these taxes at the time of purchase. Always remember, knowledge is power when it comes to tax matters!