F-14/15, Orbit Mall, Civil Lines, Jaipur-302006

F-14/15, Orbit Mall, Civil Lines, Jaipur-302006

Register & Login

Register & Login

Employee Provident Fund, commonly known as EPF, is a social security scheme introduced by the Employees' Provident Funds and Miscellaneous Act, of 1952. It is administered by the Employees' Provident Fund Organisation (EPFO), which is a non-constitutional body under the Ministry of Labour and Employment, Government of India. EPF is designed to provide financial security and stability to employees after their retirement. In this comprehensive guide, we will explore the various aspects of EPF, including its schemes, benefits, contribution details, and the process of applying for it.

What is EPF?

EPF is a mandatory savings scheme for employees working in the organized sector in India. Under this scheme, the employer and the employee contribute a certain percentage of the employee's basic salary and dearness allowance towards the EPF account. The contributions made by the employee and the employer are deposited into a permanent account linked to a Unique Account Number (UAN) assigned to each employee. The EPF account earns interest on the accumulated balance, which helps in building a significant corpus for retirement.

EPF Schemes

The EPF scheme offers three main schemes to cater to the different financial needs of employees:

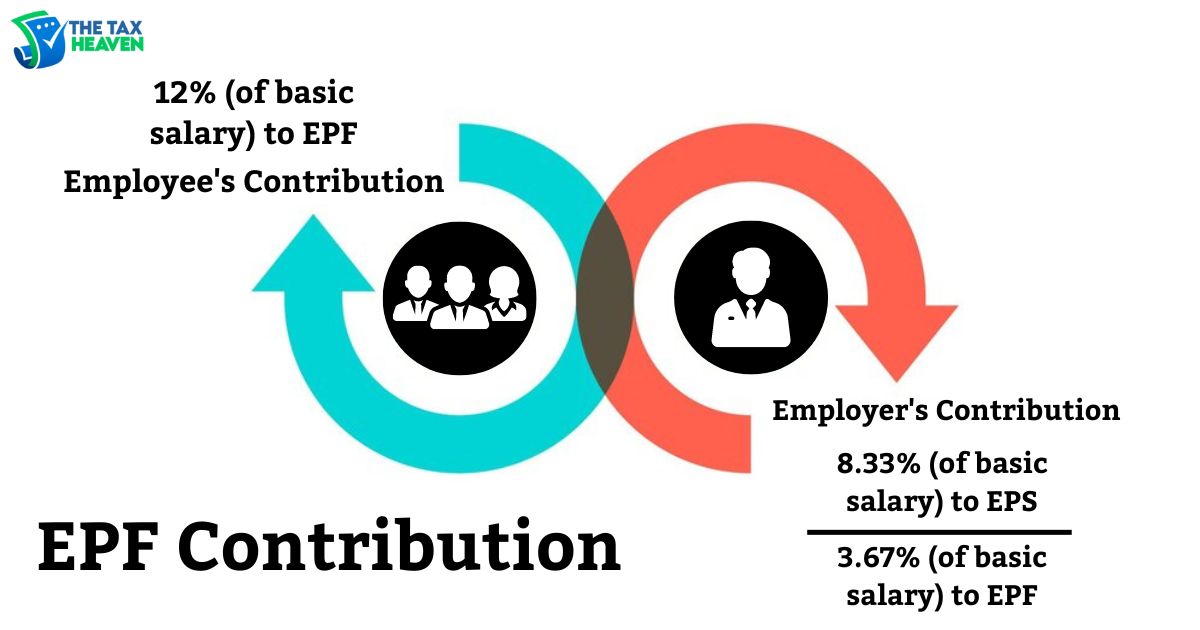

- Employees' Provident Fund Scheme 1952 (EPF): This scheme focuses on building a retirement corpus for employees. It requires the employer and the employee to contribute 12% of the employee's basic salary and dearness allowance towards the EPF account.

- Employees' Pension Scheme 1995 (EPS): EPS is a pension scheme that provides a monthly pension to employees after their retirement. The employer contributes 8.33% of the employee's basic salary towards the EPS scheme.

- Employees' Deposit Linked Insurance Scheme 1976 (EDLI): EDLI is an insurance scheme that provides life insurance coverage to employees. The employer contributes 0.50% of the employee's basic salary towards the EDLI scheme.

Benefits of Employee Provident Fund (EPF)

EP0F offers several benefits to employees, making it an essential component of their financial planning. Here are some key benefits of EPF:

Contribution to EPF

Both the employee and the employer contribute towards the EPF account. The contributions are calculated as a percentage of the employee's basic salary and dearness allowance. Currently, the contribution rate is 12% of the employee's basic salary and dearness allowance. The employer's contribution is divided into different categories, including the Employees' Provident Fund (3.67%), Employees' Pension Scheme (8.33%), Employee's Deposit Linked Insurance Scheme (0.50%), EPF Administrative Charges (1.10%), and EDLI Administrative Charges (0.01%).

How to Apply for EPF?

To apply for EPF, employees need to follow a simple process:

- UAN Generation: The employer generates a Universal Account Number (UAN) for each employee. The UAN remains the same even if the employee changes jobs.

- UAN Activation: Employees need to activate their UAN by visiting the EPFO member portal (https://unifiedportal-mem.epfindia.gov.in/memberinterface/). They can log in using their member ID and set a password.

- EPF Contribution: Once the UAN is activated, both the employee and the employer start contributing towards the EPF account. The contributions are deducted from the employee's salary and deposited into the EPF account.

- Monitoring and Withdrawal: Employees can regularly monitor their EPF balance, contribution details, and interest earned through the EPFO member portal. They can also withdraw a portion of their EPF balance for specific purposes by submitting the necessary documents and forms.

EPF Calculator: Estimating Savings for Retirement

An EPF calculator is a useful tool that helps employees estimate their savings and the corpus they can accumulate by the time they retire. It takes into account factors such as the employee's monthly salary, contribution percentage, annual salary increment, and the rate of interest on EPF deposits. By inputting these details, employees can get a clear picture of their future savings and plan their finances accordingly.

Conclusion

Employee Provident Fund (EPF) is a crucial savings scheme that provides financial security and stability to employees after retirement. With the contributions made by both the employee and the employer, along with the accrued interest, EPF helps individuals build a substantial corpus for their post-retirement years. It offers various benefits, including tax advantages, loan facilities, and insurance coverage. By understanding the EPF scheme and using tools like the EPF calculator, employees can effectively plan for their financial future and ensure a comfortable retirement